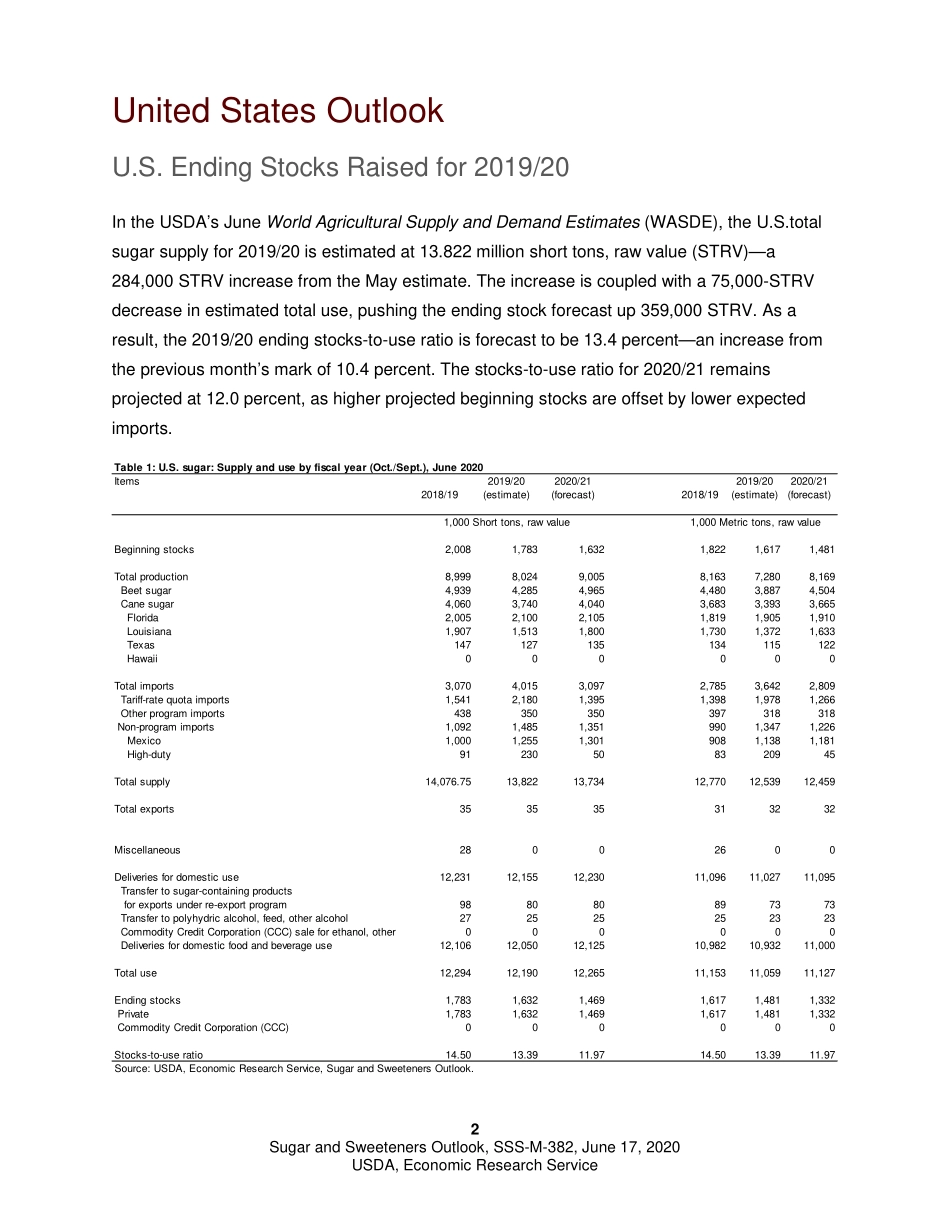

Approved by USDA’s World Agricultural Outlook Board Sugar and Sweeteners Outlook Michael McConnell, coordinator Jennifer K. Bond, contributor U.S. Sugar Market Ending Stocks for 2019/20 Raised on Higher Imports, Lower Use The U.S. sugar market in 2019/20 is estimated to have a stocks-to-use ratio of 13.4 percent, compared with 10.4 percent the previous month. Domestic deliveries are reduced 75,000 short tons, raw value (STRV) based on lower deliveries reported in April, as consumers shifted heavily toward at-home food consumption. Imports are raised 284,000 STRV from the previous month due to higher shipments from Mexico and more high-tier imports expected. Projected ending stocks for 2020/21 remain unchanged, as higher beginning stocks are offset by lower imports from Mexico. Mexico sugar production is raised 105,000 metric tons, actual value (MT) to 5.230 million MT, as the harvest is scheduled to conclude by the end of June. Domestic deliveries are lowered 70,000 MT. As a result, Mexico is forecast to have additional supplies for export to the United States for 2019/20. The global sugar market is projected to see production and consumption rebound in 2020/21 on higher field and factory yields, after poor weather conditions in several major sugar-producing countries resulted in a production deficit for 2019/20. The global sugar market will be influenced by weather, public health and domestic health policies, and macroeconomic factors such as oil prices and exchange rates, however, resulting in expected market volatility. U.S. honey production increased in 2019, but the national average price fell. Imports continue to account for most of the domestic supply, as pollinator migratory patterns follow the seasonal movement of forage areas and economic drivers.Economic Research Service | Situation and Outlook Report Next release is July 16, 2020 SSS-M-382 | June 17, 2020 In this report: U.S. Sugar Outlook Mexico Sugar Outlook Global Sugar Markets U.S. Honey Market 2 Sugar and Sweeteners Outlook, SSS-M-382, June 17, 2020 USDA, Economic Research Service United States Outlook U.S. Ending Stocks Raised for 2019/20 In the USDA’s June World Agricultural Supply and Demand Estimates (WASDE), the U.S.total sugar supply for 2019/20 is estimated at 13.822 million short tons, raw value (STRV)—a 284,000 STRV increase from the May estimate. The increase is coupled with a 75,000-STRV decrease in estimated total use, pushing the ending stock forecast up 359,000 STRV. As a result, the 2019/20 ending stocks-to-use ratio is forecast to be 13.4 percent—an increase from the previous month’s mark of 10.4 percent. The stocks-to-use ratio for 2020/21 remains projected at 12.0 percent, as higher projected beginning stocks are offset by lower expected imports. Table 1: U.S. sugar: Supply and use by fiscal year (Oct./Sept.), June 2020Items2019/202020/212019/202020/21(...